[Infographic] Independent Perspectives Prove Effective in Resolving JV Disputes

98% of disputes that have been referred to a dispute review board do not proceed to arbitration or litigation.

Exits from joint ventures are not always bad, but like death and taxes, they are usually unavoidable. Planning up front can make all the difference.

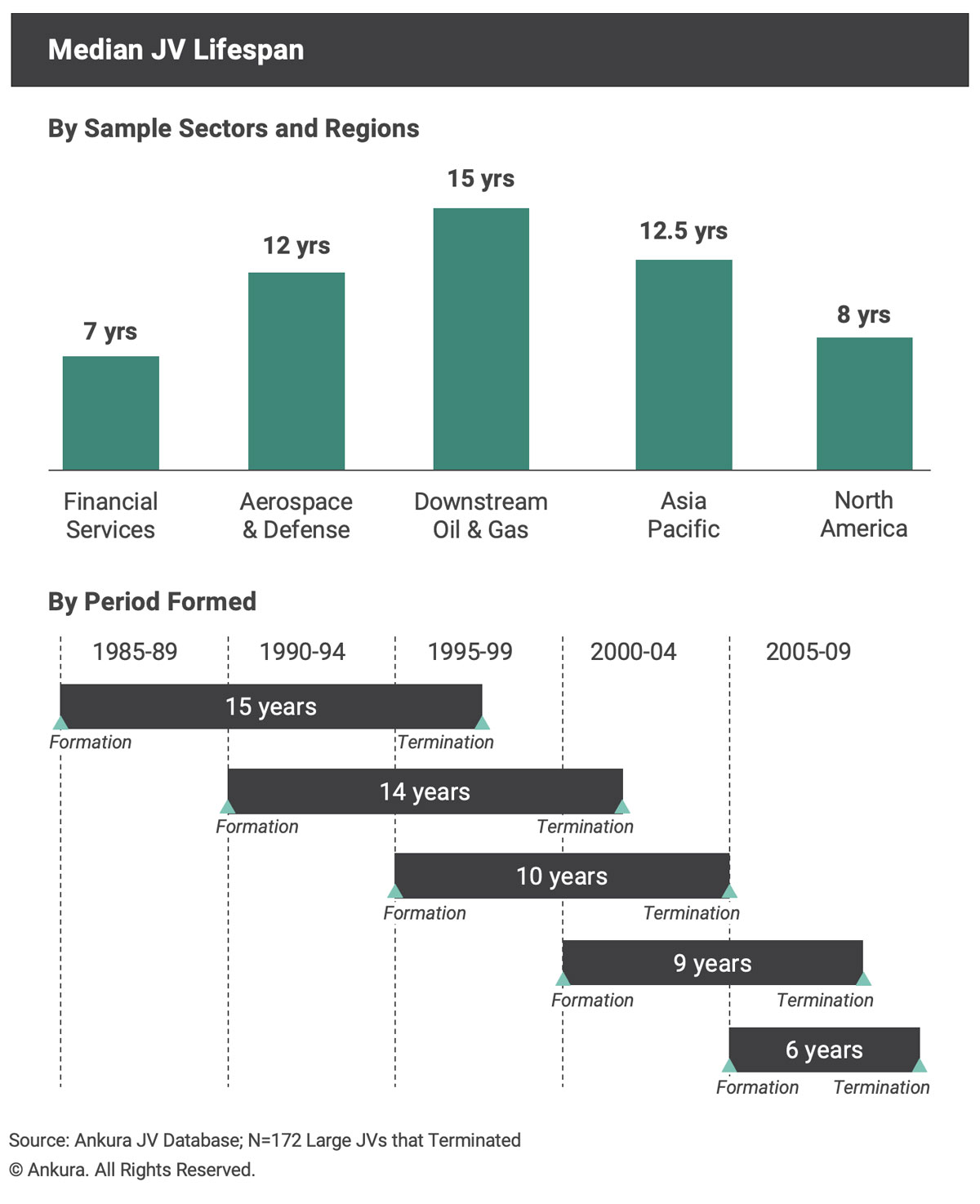

AUGUST 2020— JOINT VENTURE EXIT is a key issue for dealmakers and corporate executives whose portfolios contain material JVs spanning the globe. One way or another, companies eventually exit their JV investments – sometimes sooner than expected. Recent analysis of JV lifespan data shows that newer JVs are undergoing exits more quickly than in the past. For example, JVs formed from 1985 to 1989 tended to last about 15 years, while those formed from 2005 to 2009 lasted only 6 years (Exhibit 1). This contributes to a high volume of exits.

"*" indicates required fields

© Ankura. All Rights Reserved.

| Recent JV Exits | Exit Year |

|---|---|

| OneWeb Satellites (OneWeb-Airbus – technology) | 2020 |

| BAMS (BoA-First Data – financial services) | 2020 |

| Glencore Merafe (mining) | 2020 |

| Lake Charles LNG (Shell-Energy Transfer – energy) | 2020 |

| Onduo (Verily-Sanofi – biotech/pharma) | 2020 |

| Ambatovy (Sherritt-Korea-Sumitomo – mining) | 2020 |

| Qatar Fertilizer Company (QP-Yara) | 2020 |

| CAPSA (PSA-Changan – automotive) | 2019 |

| Fuji Xerox (Fuji-Xerox – manufacturing) | 2019 |

| IM Flash (Micron-Intel – semiconductors) | 2019 |

| Synvina (Avantium –BASF – chemicals) | 2019 |

| Arlanxeo (Saudi Aramco-Lanxess - chemicals) | 2018 |

| Daimler Ford (fuel cells) | 2018 |

| Grasberg (Rio Tinto-Freeport-Gov’t – mining) | 2018 |

| Hitachi ABB (power grid systems) | 2018 |

| MIHBV (ArcelorMittal-Macsteel – shipping) | 2018 |

| PGT Healthcare (Teva-P&G - healthcare) | 2018 |

| McDonald’s India (MIPL-CPRL – restaurants) | 2017 |

| Motiva Enterprises (Shell-Saudi Aramco – refining) | 2017 |

| Dow Corning (performance materials) | 2017 |

| Source: Ankura JV Database; N=172 Large JVs that Terminated © Ankura. All Rights Reserved. |

|

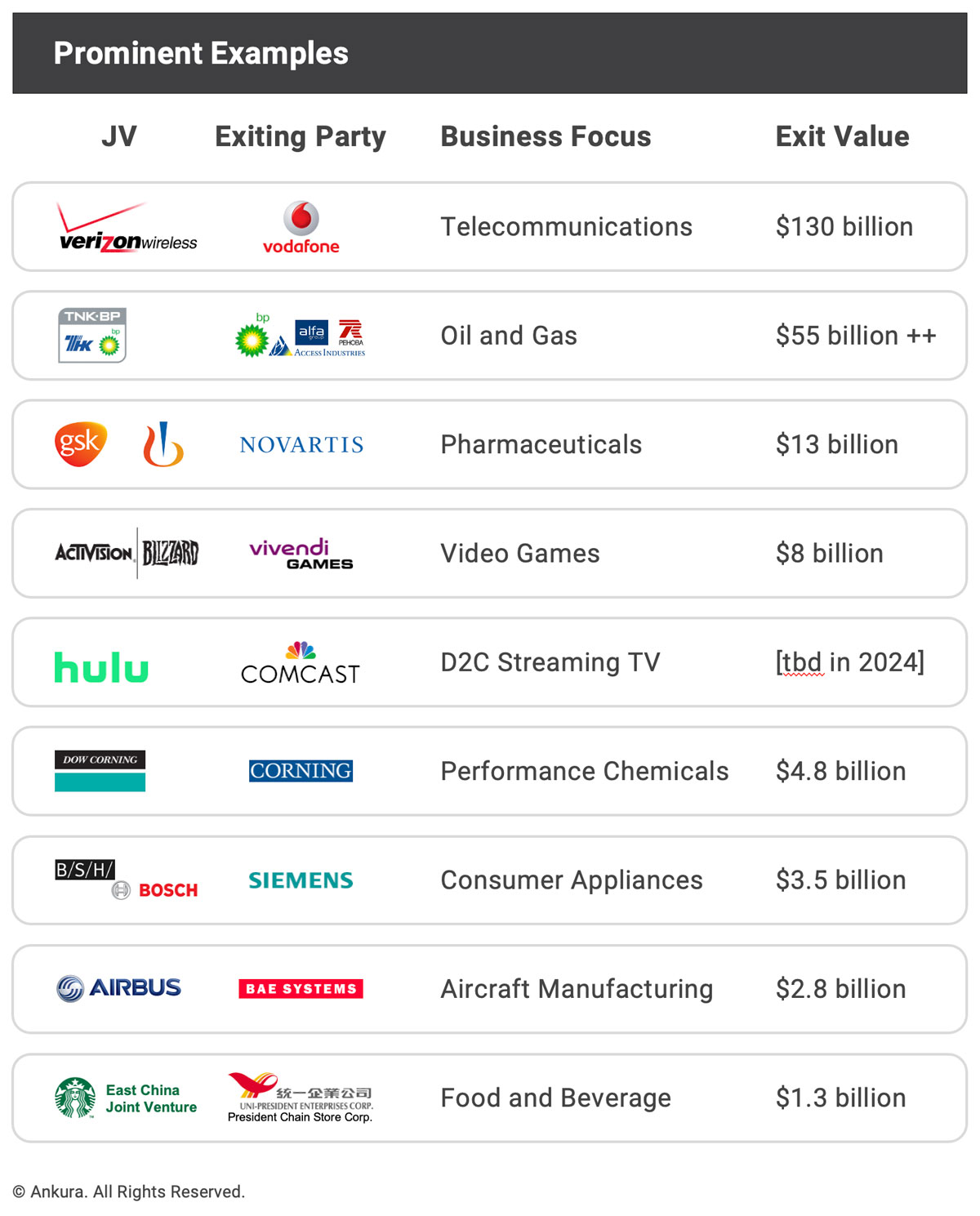

An exit, transfer, or termination event can involve significant value (Exhibit 2): Verizon paid $130 billion to buy Vodafone out of the Verizon Wireless JV; Rosneft paid $55 billion to take over TNK-BP; and GSK paid $13 billion to buy out Novartis’ 36.5% stake in their Consumer Healthcare JV. Exit deal terms are also tricky to define, let alone negotiate. There’s a huge variety of constructs to choose from, and a lot of mental chess that goes into it. Even the slightest misstep in deal structuring can “box in” executives that inherited the JV when they seek to exit down the road.

Yet exit terms are often the last topic of discussion for dealmakers when structuring new deals. And little attention has been paid to codifying the art and science of these terms – or how to implement the exit process, on the back end. This is a mistake, because JV exits can have big winners and losers. And they can be messy, sometimes with adverse press coverage.

The balance of this article addresses two issues:

To craft JV exit terms, dealmakers must consider exit triggers (i.e., conditions under which one party can initiate an exit decision), disposition approaches (such as selling to a partner or taking the JV public), rights / restrictions on transfer (such as a “call option” or “buy-sell” agreement, etc.), and lastly, valuation mechanics.[1]Other related provisions may include post-exit obligations and liabilities (e.g., non-compete; transferability of assets/IP; post-exit services), voting matters, dispute, and deadlock procedures.

Based on an analysis of over 70 JV contracts, and prior experience with hundreds of JVs, we offer five best-practices for JV dealmakers contemplating exit provisions:

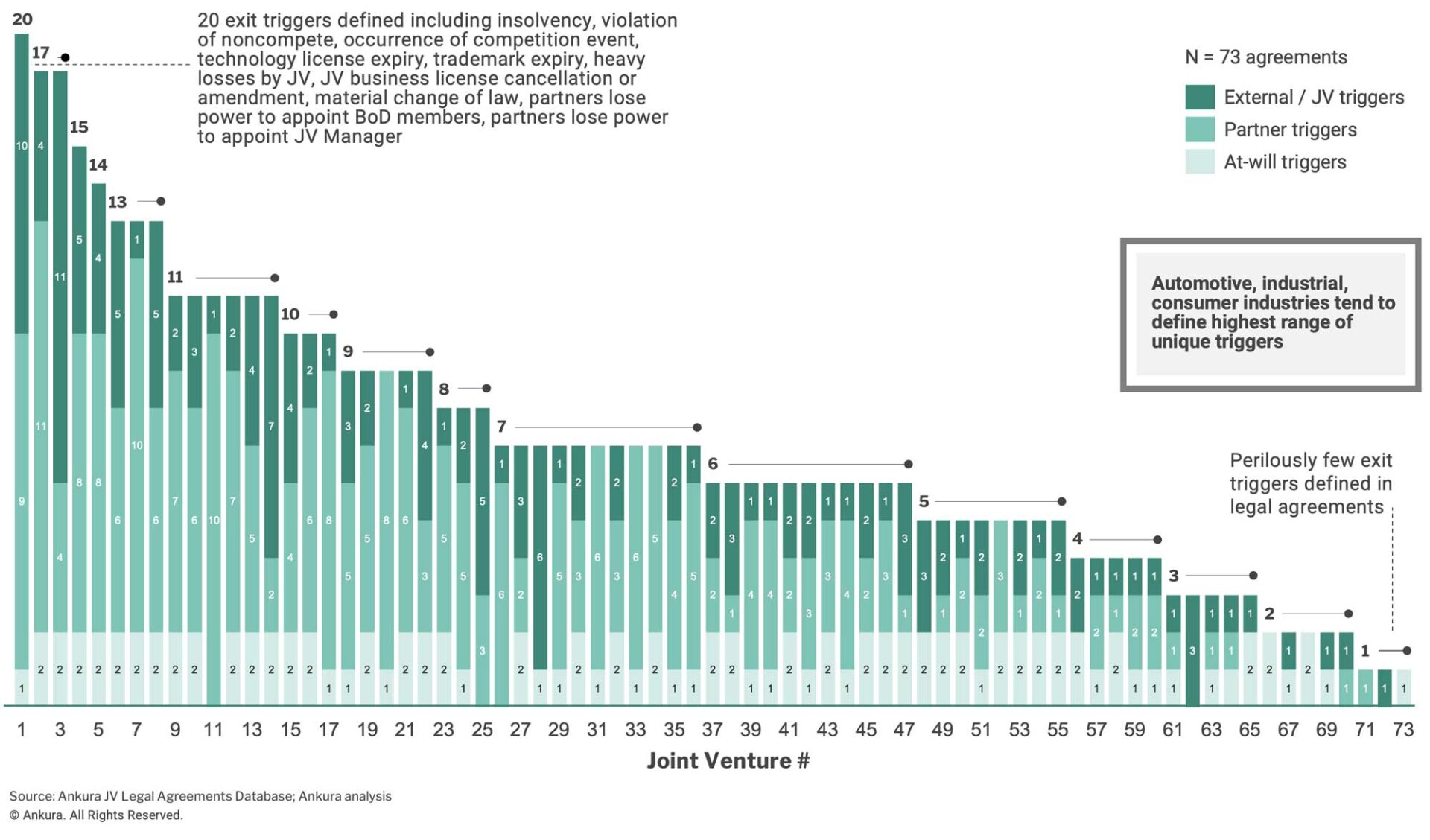

Our analysis indicates that there is a huge dispersion in the number of exit triggers, with 25% of JVs having four or fewer triggers (Exhibit 3).

We believe that all JVs should have four basic exit triggers: a) partner default / bankruptcy; b) uncured breach of contract (including failure to provide assets or resources that were committed to the JV); c) partner change of control to a competitor; and d) insolvency of the JV.

The vast majority of JVs should have more than these basic four exit triggers.

Specifics differ according to the deal context, but triggers to consider include (Exhibit 4):

In most JVs, there is a “natural buyer” and a “natural seller.” Few JVs are true partnerships of equals – or, if they start that way, a natural buyer / seller emerges over time. This happens because one of the partners has deeper pockets, stronger capabilities, or is winning the “race to learn” in the venture, and as a result becomes a more natural owner of the venture as time goes on. Similarly, it’s usually true that the moment of greatest negotiation power for one of the partners is the day they sign the JV agreement.

This dynamic has a huge implication for setting up exit provisions. In joint ventures where one of the partners isn’t able to operate the JV independently, a boilerplate buy-sell agreement in which one partner writes down a price at which the other can buy or sell, tremendously disadvantages the weaker partner. The buyer can offer an artificially low price, confident that the partner will have little choice other than to accept. Also, every company who thinks they might be a natural seller should adopt the approach of having an external valuation to determine the selling price, rather than relying on negotiation.

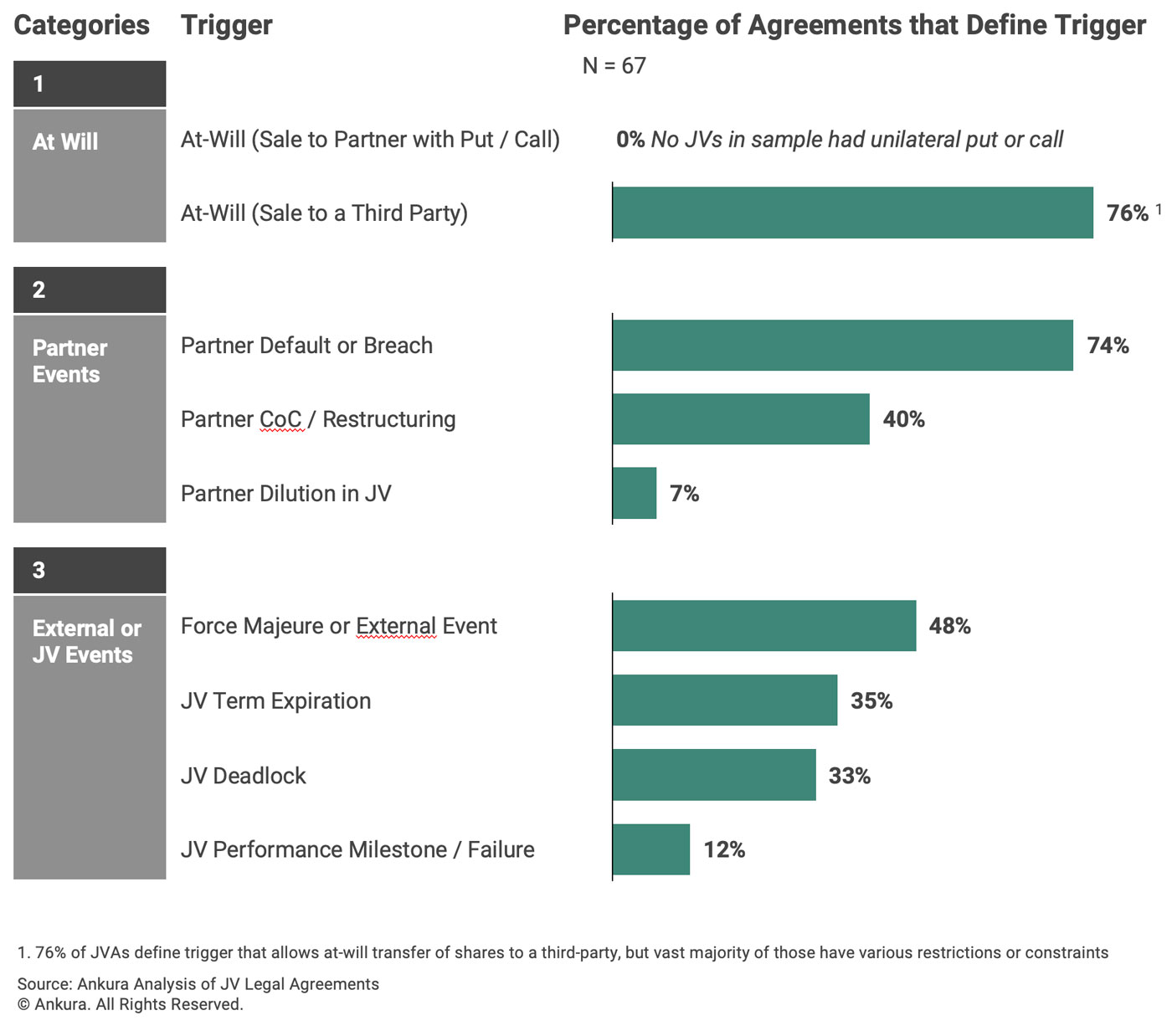

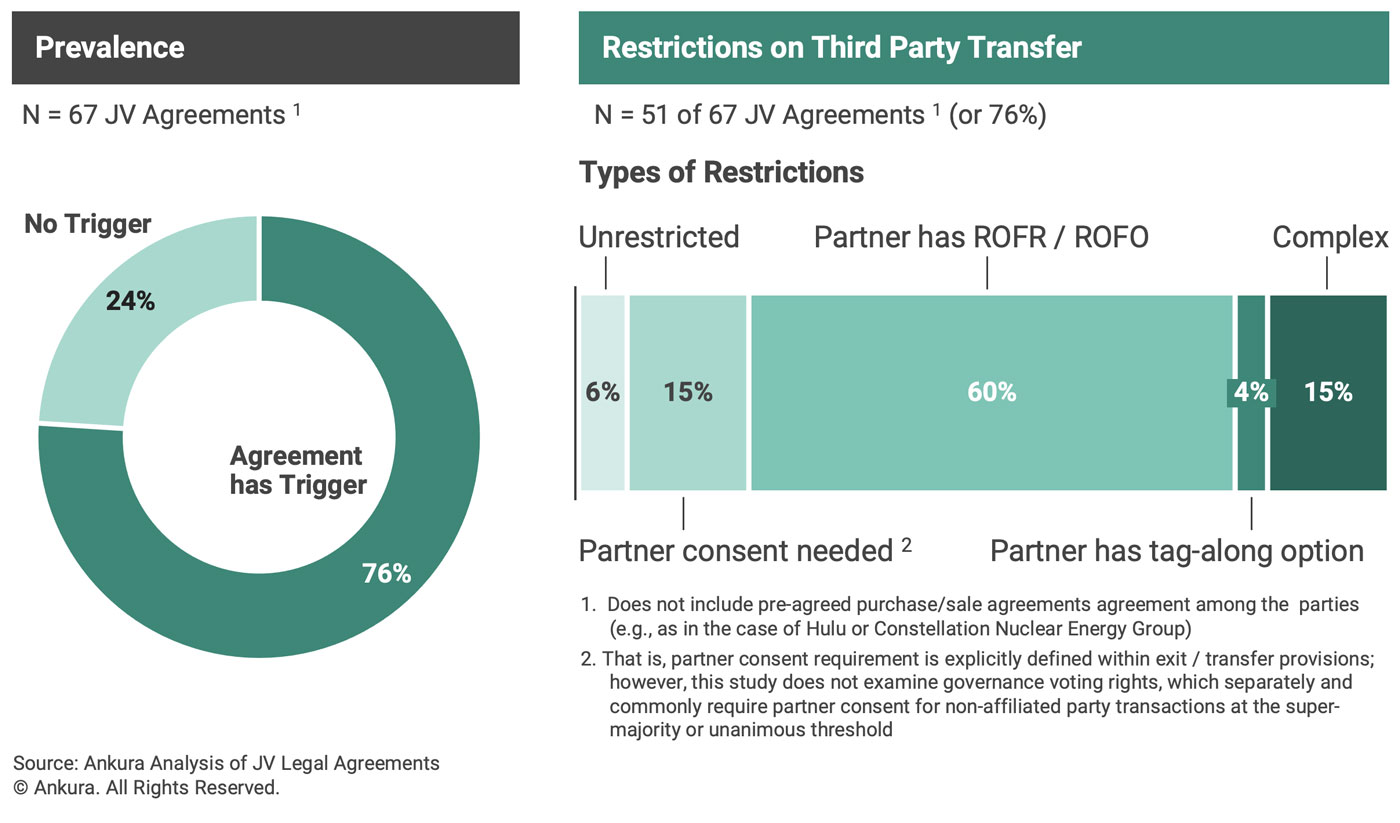

Our examination of 67 JV agreements indicates that approximately three-quarters of JVs have a clause allowing at-will transfer of a partner’s interest to a third party. However, most ventures have serious restrictions that undercut the value of this clause for potential sellers (Exhibit 5). Specifically, fully 60% of JVs have a ROFR (right of first refusal) or ROFO (right of first offer) – more often a ROFR, which makes selling to a third party very tough. Who wants to go through due diligence, negotiations, and legal drafting, spending valuable management time and legal fees, only to face double jeopardy that the other JV partner can step in and take over the deal?

To avoid this, dealmakers should consider ROFO instead of ROFR clauses. They should also set up the JV with limited use of parent company services, with arms-length pricing on services, inputs and support from parents – or a path to achieve these things – and avoid, if possible, the JV being a captive buyer or supplier from parent companies in perpetuity. It’s also important to write in continuation of service provisions ensuring that the JV will have access to any important parent-company services, inputs, or support for at least 18-24 months following a buyout.

In theory, certain JVs can be set up so that they are on a track to IPO or sell the entire JV to a strategic buyer, as a way to monetize investments. This requires a high degree of autonomy; an external market facing orientation; limited reliance on parent secondees, services, inputs, or capabilities; and exit clauses that allow one of the shareholders to trigger an IPO process or full JV sale when certain milestones are reached2. In practice, these types of truly independent ventures are a rare breed.

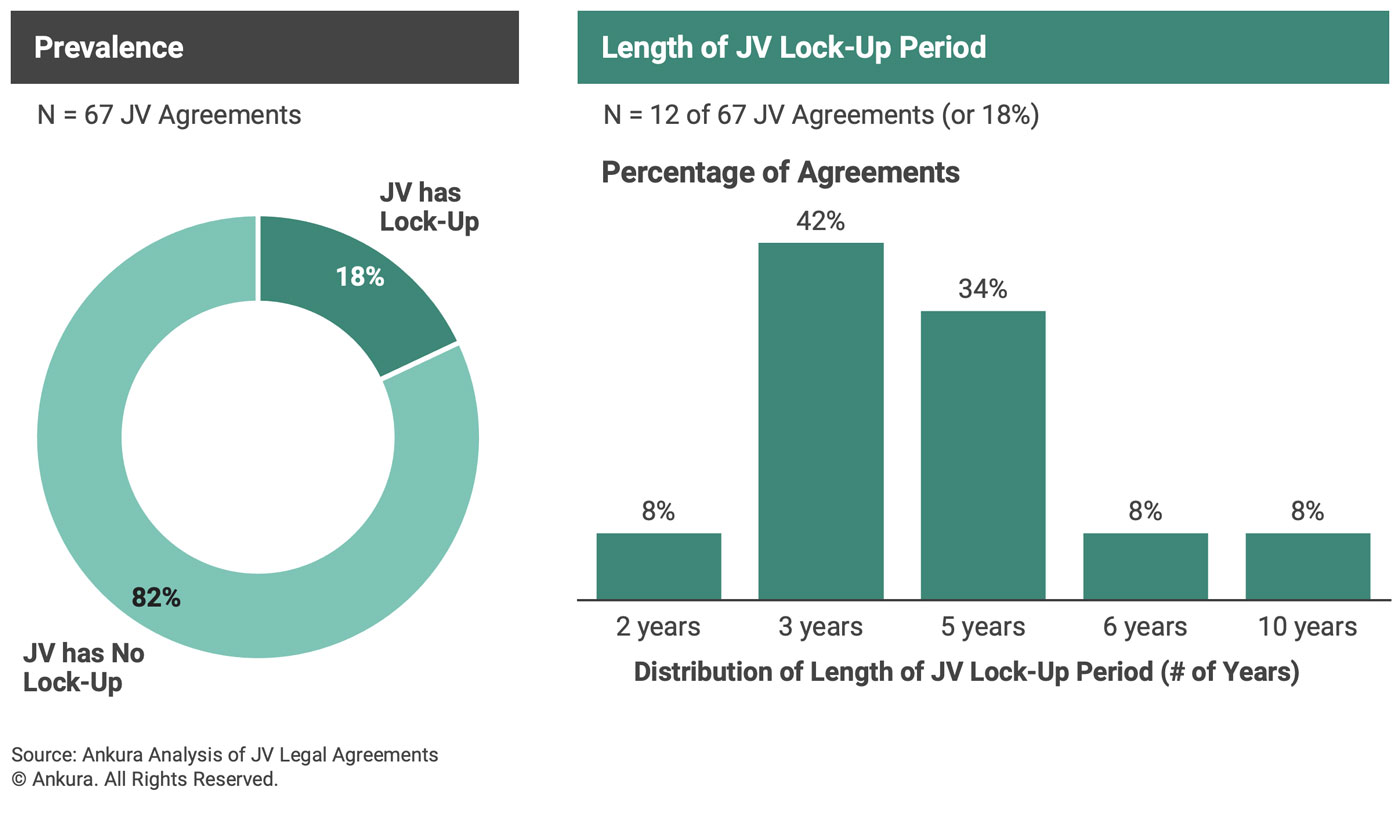

Only 18% of JVs have a lock-up period specified in their JVA, with a median term of 4 years (Exhibit 6). Our view is that many JVs would benefit from a 2- to 5-year lock-up period, during which both parents are committed to the JV and follow through on delivering the agreed commitments to the JV. This can insulate JVs from the usual bumps that can happen in the early years.

One-third of JVs specify that a Board deadlock on certain issues will trigger termination, following a dispute-resolution approach. When this happens, the most common exit mechanism is a put or call mechanism. Another third of JVs have a deadlock process that doesn’t explicitly lead to exit, and fully one-third of JVs don’t have a defined approach to dealing with deadlock at all.

In our view, most JVs should link a limited number of deadlock issues to termination. For example, continued inability to approve a new budget or capital program, if continued beyond 6-12 months, can have a substantial adverse impact on the JV’s operations. These issues are not ones where outside arbitration is appropriate, as they are business judgements – therefore if unresolved, they should lead to an exit process. However, some JVs have an overly long list of disputes that can trigger exits, including disagreement on M&A, disagreement on strategic plan, naming of the CEO, disagreement on dividend/ distribution policy and so on. Our view is that many of these issues can be defused by pre-agreeing on policies, or having non-agreement lead to retaining the status quo ante. One cross-cutting caveat: dealmakers should always tailor exit terms to the specific JV context.

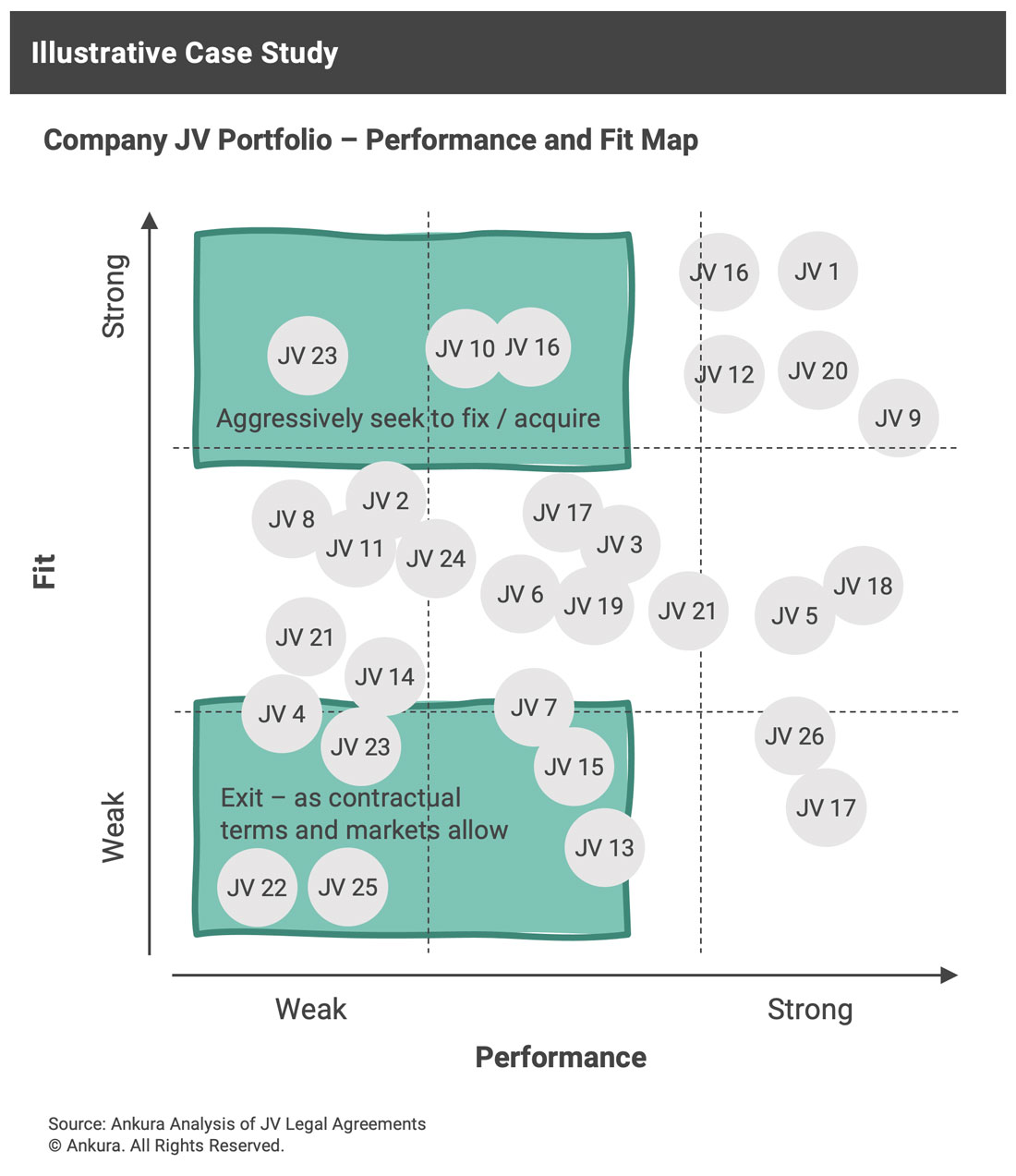

In a perfect world, executives would regularly review their JV portfolios to assess individual JV performance and fit with the parent company’s forward-looking strategy (Exhibit 7). Based on this, companies should proactively seek to restructure, where feasible, or to acquire or sell down investments in JVs. JVs with poor performance and strong fit can be restructured, if possible; otherwise they can be acquired and turned around. JVs with strong performance and strong fit may be good acquisition candidates, unless the partners continue adding value to the JV. JVs with poor fit are candidates for sale.

John Steinbeck famously said, “I see too many men delay their exits with a sickly, slow reluctance to leave the stage. It’s bad theater as well as bad living.” It’s important to be proactive in restructuring or exiting JVs when the time comes. If you don’t, your partner might beat you to the punch.

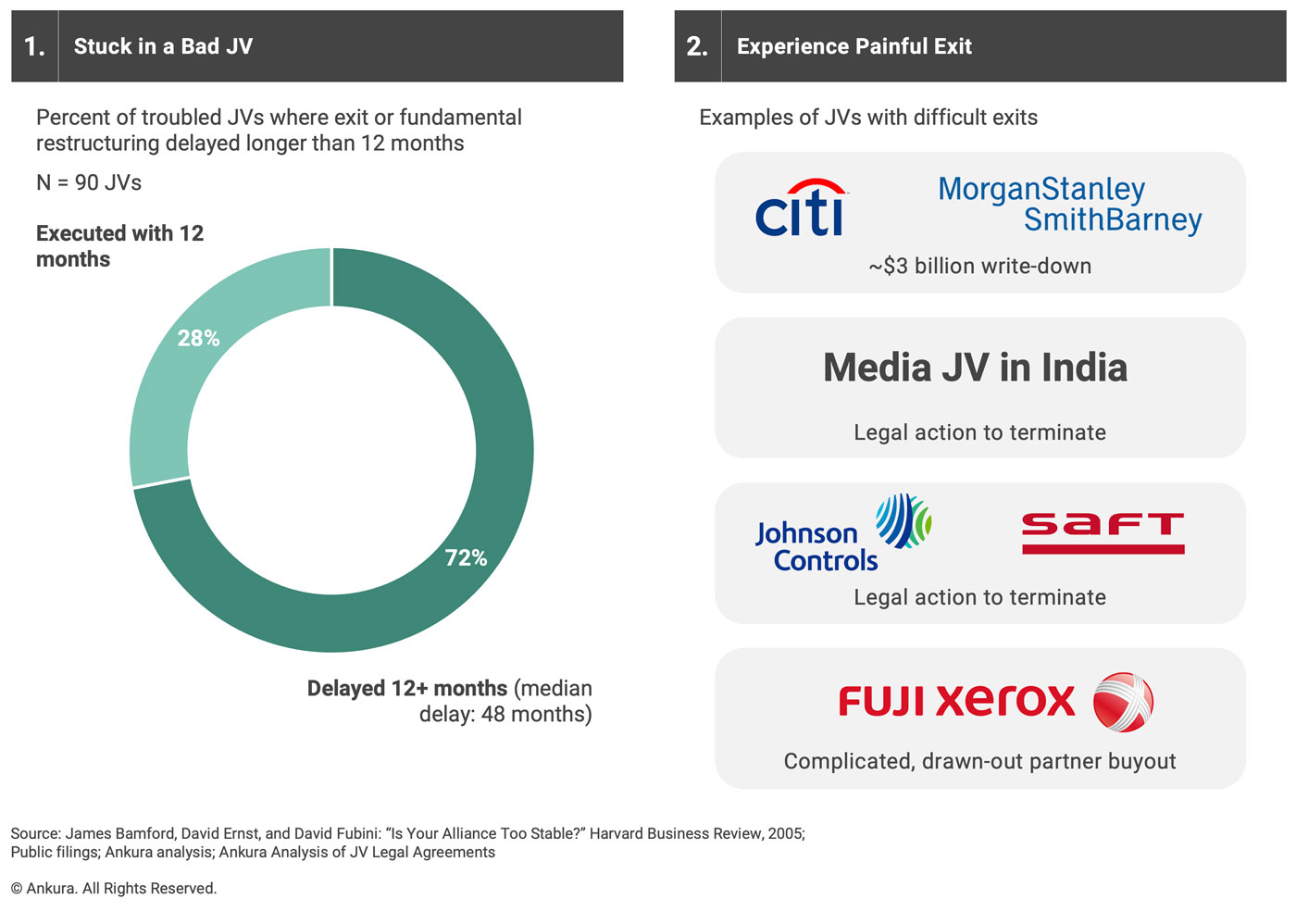

In reality, the path to exiting a JV is challenging. Unfortunately, many executives find themselves in a position where they wish to exit, but have no clean, unilateral ability to do so. Fully 72% of troubled JVs undergo an exit or restructuring that is delayed by more than one year. And when exit or restructuring finally occurs, it is often painful, with bad press, legal fees, and exit prices that destroy shareholder value (Exhibit 8).

Consider the case of a media JV in India, where a global player had set up a JV with a local player, aiming to grow the business. Each of the parent companies had committed that the JV would be their exclusive channel in India. The business was underperforming in a fast-growing market, and needed investment to keep share, let alone grow relative to competitors. However, the Indian partner was unable to invest, and unwilling to take on debt and didn’t approve investments proposed by the JV management team. The global partner made a fair offer to buy out the Indian partner, but this offer was rejected.

Perhaps the Indian partner realized that the value to the global partner of owning the JV outright was greater than that implied by an external “fair market” valuation – a situation that is not uncommon for wily local players. In the end, the global partner ended up paying a high price to buy out the JV to regain its freedom to operate in India, one of its most important markets for expansion.

How to avoid these twin perils? The best answer is to structure exit clauses up front, along the lines of our advice above. But, if you have inherited one or more JVs that is already on a path toward unwind, here’s a blueprint to How to avoid these twin perils? The best answer is to structure exit clauses up front, along the lines of our advice above. But, if you have inherited one or more JVs that is already on a path toward unwind, here’s a blueprint to get you running for the exits. Companies should generally follow a three-step process to prepare for and execute exit negotiations (Exhibit 9).

Source: Ankura Analysis of JV Legal Agreements

© Ankura. All Rights Reserved.

Exits from joint ventures aren’t always painful, or bad, but like death and taxes, they are usually unavoidable. Planning up front can make all the difference.

We understand that succeeding in joint ventures and partnerships requires a blend of hard facts and analysis, with an ability to align partners around a common vision and practical solutions that reflect their different interests and constraints. Our team is composed of strategy consultants, transaction attorneys, and investment bankers with significant experience on joint ventures and partnerships – reflecting the unique skillset required to design and evolve these ventures. We also bring an unrivaled database of deal terms and governance practices in joint ventures and partnerships, as well as proprietary standards, which allow us to benchmark transaction structures and existing ventures, and thus better identify and build alignment around gaps and potential solutions. Contact us to learn more about how we can help you.